Backtesting is crucial for evaluating the AI stock trading predictor's potential performance by testing it on historical data. Here are 10 useful strategies to help you evaluate the results of backtesting and verify that they are accurate.

1. Insure that the Historical Data

Why is it important to test the model using a a wide range of market data from the past.

Verify that the backtesting period is encompassing multiple economic cycles over many years (bull flat, bear markets). This allows the model to be tested against a wide range of conditions and events.

2. Confirm the realistic data frequency and degree of granularity

The reason the data must be gathered at a frequency that matches the trading frequency intended by the model (e.g. Daily or Minute-by-60-Minute).

What are the implications of tick or minute data are required for the high-frequency trading model. Long-term models can depend on weekly or daily data. Inappropriate granularity can cause inaccurate performance data.

3. Check for Forward-Looking Bias (Data Leakage)

What is the reason? By using future data for past predictions, (data leakage), the performance of the system is artificially enhanced.

Make sure that the model is using only the data that is available for each time point during the backtest. Look for safeguards like the rolling windows or cross-validation that is time-specific to ensure that leakage is not a problem.

4. Evaluate Performance Metrics Beyond Returns

Why: A focus solely on returns may obscure other risk factors.

The best way to think about additional performance indicators, including the Sharpe ratio, maximum drawdown (risk-adjusted returns) as well as the volatility, and hit ratio. This will provide a fuller image of risk and consistency.

5. Evaluation of the Transaction Costs and Slippage

Why is it important to consider slippage and trade costs could result in unrealistic profit targets.

How: Verify the backtest assumptions are real-world assumptions regarding spreads, commissions and slippage (the price fluctuation between order execution and execution). Small differences in costs can be significant and impact results for high-frequency models.

Review the Position Size and Management Strategies

The reason: Proper risk management and position sizing impacts both exposure and returns.

What to do: Check that the model is governed by rules governing position sizing which are based on risks (like the maximum drawdowns in volatility-targeting). Make sure that backtesting takes into account diversification and risk-adjusted sizing not only absolute returns.

7. Always conduct cross-validation or testing out of sample.

Why: Backtesting based solely on the data in the sample could result in overfitting. This is where the model does extremely well when using data from the past, but doesn't work as well when it is applied in real life.

Utilize k-fold cross validation or an out-of-sample time period to assess generalizability. Testing out-of-sample provides a clue for the real-world performance using unseen data.

8. Analyze model's sensitivity towards market rules

Why: The behaviour of the market could be influenced by its bear, bull or flat phase.

How to: Compare the outcomes of backtesting across different market conditions. A well-designed, robust model must either be able to perform consistently in different market conditions, or incorporate adaptive strategies. Positive indicator Performance that is consistent across a variety of environments.

9. Consider the Impact Reinvestment or Complementing

Reason: Reinvestment strategies could increase returns when compounded unintentionally.

How to: Check whether backtesting is based on realistic compounding assumptions or Reinvestment scenarios, like only compounding a small portion of gains or investing the profits. This will prevent inflated results due to exaggerated reinvestment strategies.

10. Verify the reproducibility results

Why? The purpose of reproducibility is to guarantee that the outcomes aren't random but consistent.

How: Confirm whether the same data inputs can be used to duplicate the backtesting process and generate the same results. The documentation must be able to produce identical results across different platforms or in different environments. This will give credibility to your backtesting method.

These tips will allow you to evaluate the accuracy of backtesting and improve your understanding of an AI predictorâs potential performance. It is also possible to determine if backtesting produces realistic, reliable results. Take a look at the top rated ai penny stocks recommendations for more examples including best ai stocks to buy now, stock trading, stock analysis ai, market stock investment, ai stock, ai stock trading app, market stock investment, stock market, playing stocks, openai stocks and more.

10 Tips For Evaluating The Nasdaq Composite By Using An Ai Prediction Of Stock Prices

When evaluating the Nasdaq Composite Index, an AI stock prediction model must take into account its unique features and elements. The model must also be able to precisely analyze and predict the movement of the index. Here are ten tips to evaluate the Nasdaq Composite with an AI Stock Trading Predictor.

1. Understand Index Composition

What's the reason? The Nasdaq Composite includes more than three thousand companies, with the majority of them in the technology, biotechnology and internet sector. This is different from an index that is more diverse such as the DJIA.

Begin by familiarizing yourself with the businesses that are the largest and most influential in the index. This includes Apple, Microsoft and Amazon. Knowing their significance can assist AI better predict the direction of movement.

2. Include sector-specific factors

What's the reason? Nasdaq market is heavily affected by technology and sector-specific changes.

How to include relevant elements into your AI model, for example, the performance of the tech sector, earnings reports or trends in both hardware and software sectors. Sector analysis can improve the predictability of the model.

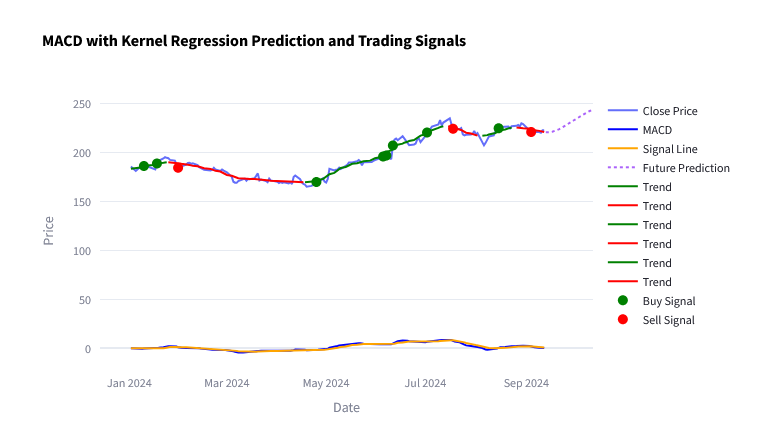

3. Use of Technical Analysis Tools

Why: Technical indicator assist in capturing sentiment on the market, and also the trend of price movements in an index as dynamic as Nasdaq.

How to incorporate technical tools like Bollinger Bands or MACD in your AI model. These indicators can help you identify the signals to buy and sell.

4. Monitor the impact of economic indicators on tech Stocks

The reason is that economic factors like unemployment, rates of interest and inflation are all factors that can significantly influence tech stocks.

How to integrate macroeconomic variables that are relevant to technology, like consumer spending, tech investing developments, Federal Reserve policies, and so on. Understanding these relationships will aid in improving the model.

5. Evaluate the Impact of Earnings Reports

The reason: Earnings reports from major Nasdaq firms can cause substantial price fluctuations, and impact index performance.

How to accomplish this: Ensure that the model is synchronized with earnings calendars. Refine predictions according to these dates. You can also improve the accuracy of predictions by analyzing the reaction of historical prices to announcements of earnings.

6. Technology Stocks Technology Stocks: Analysis of Sentiment

The reason: Investor sentiment may significantly influence the price of stocks especially in the tech sector, where trends can shift rapidly.

How can you include sentiment analyses from social media, financial reports and analyst rating into AI models. Sentiment analysis can provide more background information and boost predictive capabilities.

7. Conduct backtesting with high-frequency data

What's the reason: The Nasdaq is known for its volatility, making it essential to test predictions against data from high-frequency trading.

How can you use high-frequency data for backtesting the AI model's predictions. This helps validate its effectiveness under various conditions in the market and over time.

8. Evaluate the model's performance over market corrections

The reason is that Nasdaq is susceptible to sharp corrections. Understanding how the model works in downturns, is essential.

How do you evaluate the model's past performance in significant market corrections, or bear markets. Stress tests will show its resilience and ability in unstable times to reduce losses.

9. Examine Real-Time Execution Metrics

Why: An efficient trade execution is essential to making money in volatile markets.

How to track performance metrics, such as slippage and fill rate. How well does the model forecast the best entry and exit locations to Nasdaq trading?

Review Model Validation Using Ex-Sample Testing Sample Testing

Why? Out-of sample testing is a way to verify whether the model can be extended to unknowable data.

How do you conduct rigorous tests out of samples with historic Nasdaq Data that wasn't used during training. Comparing the actual and predicted performance will ensure the model is accurate and reliable.

Check these points to determine the ability of a stock trading AI to forecast and analyze the movements of the Nasdaq Composite Index. This will ensure it stays up-to-date and accurate in the changes in market conditions. Have a look at the top ai stock market hints for blog info including trading ai, ai for stock trading, investment in share market, investing in a stock, ai investment stocks, stock trading, ai stock market, investing in a stock, best stocks in ai, investment in share market and more.